Last week* we reflected on the trillions of dollars of government stimulus and monetary support that has left the United States awash in cash.

The result of all of this has undoubtedly aided the rise in risk assets during the first few months of 2021, and has led to some speculative market actions that, to us, are reminiscent of the late-1990’s dotcom bubble. By way of example:

- Leadership of loss-making companies: As readers may recall, the latter stages of the dotcom bubble were marked by nascent companies, in many cases with barely more than a business plan, coming public at multi-billion-dollar market caps and with valuations being rationalized by clicks, page views, or some similar metric. Similarly, the first two months (especially) of 2021 saw loss-making companies lead the market...in many cases being up hundreds of percent through February. For example, within the Russell 3000 Index, companies that reported losses over the trailing 12 months were up, on average, over 20% for the first two months of the year, while profit-reporting companies gained on average only 9%. More striking, the top 20 gainers in the index (each one in the loss-making category) were up an average of 226% - with every one of them appreciating over 100% for the first two months of the year.

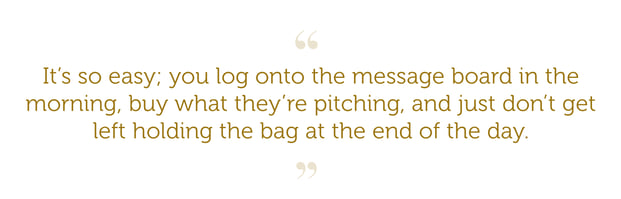

- Rise of the retail trader: In January, a group of heavily shorted stocks saw rapid price appreciation, driven largely by investors organizing on Reddit message boards in an effort to cause short squeezes, and thus dramatic increases in the prices of those stocks. This casino-like atmosphere was seemingly made easier by the rise of commission-less trading on apps such as Robinhood – giving traders the ability to transact endlessly at zero cost. As an acquaintance of ours who works in the restaurant industry, but was engaging in this trading activity, put it:

“It’s so easy; you log onto the message board in the morning, buy what they’re pitching, and just don’t get left holding the bag at the end of the day.”

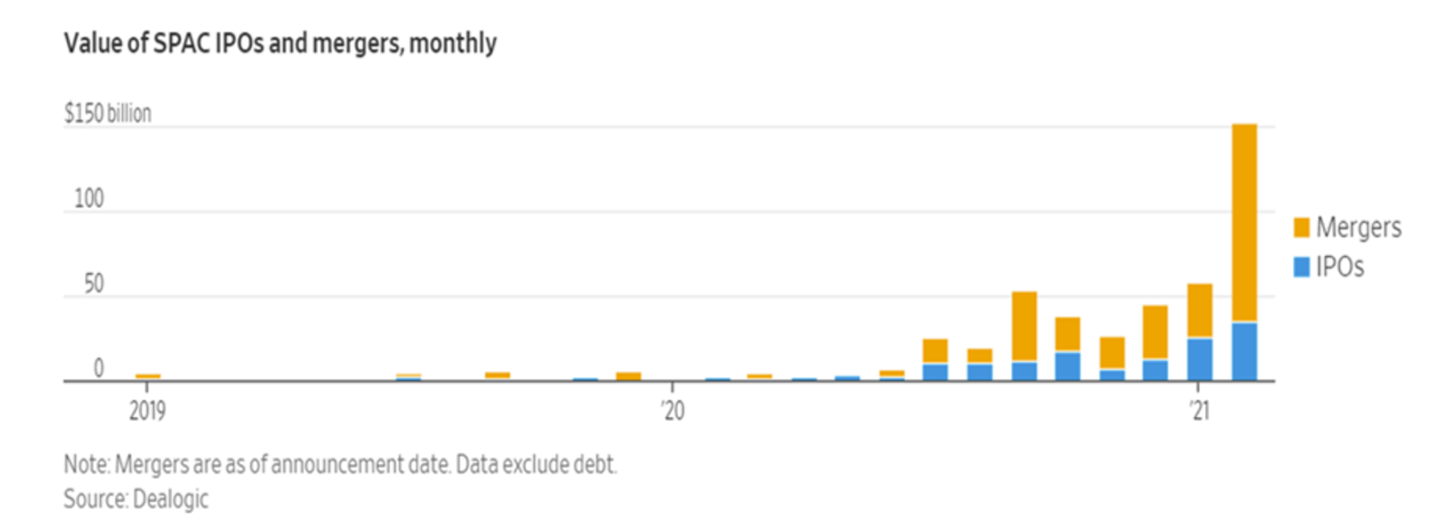

GameStop (GME), which became the “poster child” of this movement, saw its shares rise from a price of around $20 per share to a high of $483 in a matter of days and, echoing the period of the dotcom bubble, high profile investment managers could be seen on CNBC rationalizing the head-scratching valuations of these companies. - “Blank check” companies: More formally known as SPACs (special purpose acquisition companies), have quickly risen to prominence as a preferred way for private companies to IPO with less red tape and cost. As the “blank check” moniker implies, these are public companies which raise capital from investors with the promise to eventually find a private company to purchase with those funds. Typically, this must be done within a two-year period, or the money is returned to shareholders.

In just the first three months of 2021, literally hundreds of these SPACs have raised billions of dollars from investors and most of them are still looking for private companies to purchase. This didn’t stop many of them rising considerably above their IPO price, despite it being unknown what investors were really buying at the time. According to the Wall Street Journal (WSJ), at the end of March there were 430 SPACs looking for acquisition targets.

Much like dotcom companies at the turn of the century seemed to fall under the weight of too much supply, as IPO after IPO came to market and 180-day lock ups expired, causing a flood of investors to look for the exits, the SPAC market risks a similar outcome. Indeed, after seeing average gains of over 5% in January and February (and 231 consecutive SPACs going public without dipping below their IPO price), the WSJ reported that SPACs rose merely 0.1% upon their debuts during March.

- Nonfungible tokens (NFTs) and digital currencies: Next on the list of hard-to-value assets that saw billions of dollars of money flow to during the first few months of 2021 are NFTs and digital currencies. While the long-term prospects of both of these types of assets could be debated, assessing a proper valuation to either of them currently comes down to “whatever the next person is willing to pay me.” And much like the aforementioned loss-making companies, these two asset classes were caught up in the speculative frenzy which marked early 2021.

For example, Bitcoin, which started the year just under $30,000, rallied to just under $60,000 at quarter end. And NFTs, which are simplistically described as files which are attached to, and verify the authenticity of, any digital item (such as a video or music file, a GIF or a meme, etc.) were being auctioned for exorbitant sums. As an example, the first tweet ever, from Twitter cofounder Jack Dorsey was sold for a whopping $2.9 million (if you don’t want to dole out that sort of cash, feel free to scroll back to March 21, 2006 to see that tweet by @jack for yourself in his Twitter timeline)!

*If you are interested in reading last week's post, Reflections on Value’s Outperformance and Our Outlook Going Forward, click here.