Cases of whiplash must have spiked lately. In a few short months, market commentators have abruptly transitioned from: “inflation is transitory” to “inflation might be more persistent” and now “prepare for stagflation!”

So what’s behind the change in sentiment?

While concerns over a Delta-variant induced slowdown have abated somewhat, supply bottlenecks around the world have become markedly worse as demand for goods has outpaced the ability to get those goods to market. Part of the blame has been placed on a lack of truckers to transport the goods. It was recently reported that nearly half a million cargo containers were sitting off the coast of California as cargo ships are waiting to be offloaded – with some potentially waiting for a month. This not only puts the Christmas shopping season at risk for retailers, but has also already led to an increase in the price of many goods.

Meanwhile, energy prices around the world have taken off, also due to supply/demand imbalances. For example, liquefied natural gas prices (heavily relied upon in Europe and Asia) have skyrocketed on those continents to $40/mmbtu from $6/mmbtu in late February, while oil has been driven up to over $80 a barrel, from near $50 at the beginning of the year.

While most of these supply issues will prove to be temporary, the inflationary impacts may well be more persistent – especially if labor shortages lead to wage increases, which tend to be sticky. Going forward, a key question is whether these inflationary pressures will cause enough demand destruction to lead to stagflation.

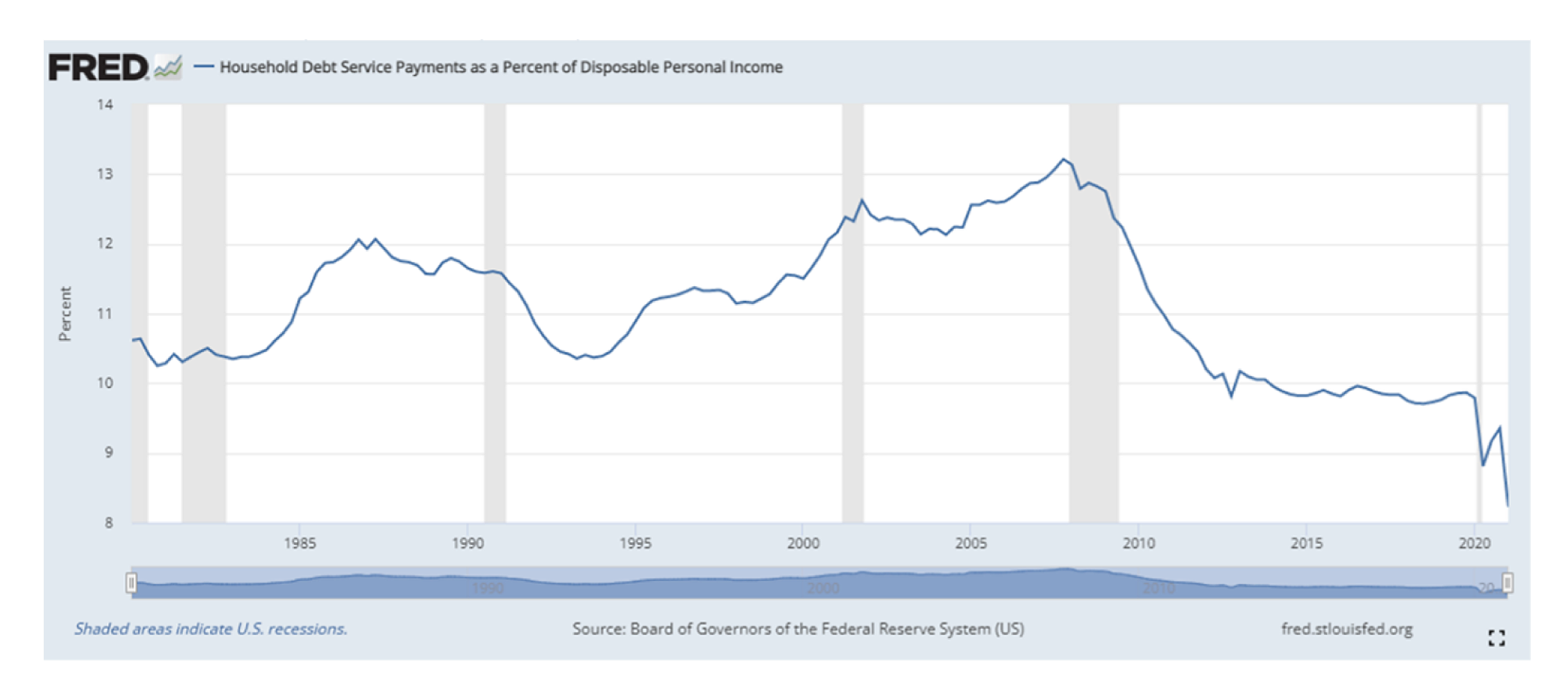

While we do not purport to be economists, we do take some comfort in the overall health of the consumer. As can be seen in the chart below, the U.S. consumer’s balance sheet is currently in great shape, with debt service as a percentage of disposable personal income at record lows. This has undoubtedly been aided by massive government stimulus and should help consumers withstand this period of rising cost pressures much more readily than they would have, say, a decade ago.

What are the Market Implications?

Given the recent concerns, it is appropriate to consider the portfolio implications if we are indeed headed towards a period of persistent inflation and stagnant economic growth. While no two periods are directly comparable (for example, the environment today is very different than that of the 1970s, when we last saw stagflation), we would expect defensive sectors such as consumer staples and healthcare to outperform given their more stable business models and ability to exhibit pricing power.

We would also expect a general flight to quality, including the outperformance of companies with above-average balance sheet strength. Notably, Morgan Stanley recently issued a report which looked at periods in which “…markets assigned a non-trivial probability to stagflation as a tail risk...” Their data showed that defensive sectors did indeed outperform during these periods, as did energy. In addition, credit spreads widened as fears of stagflation entered public discourse, adding credence to our belief that quality would outperform in such an environment. Also worth noting: according to work performed by RBC, banks outperformed through three stagflationary periods during the 1960s and 1970s.

Editor’s note: The blog below is an excerpt (lightly edited) from our Q3 client letter that was published in October 2021. We believe the information remains relevant at the time of publishing.