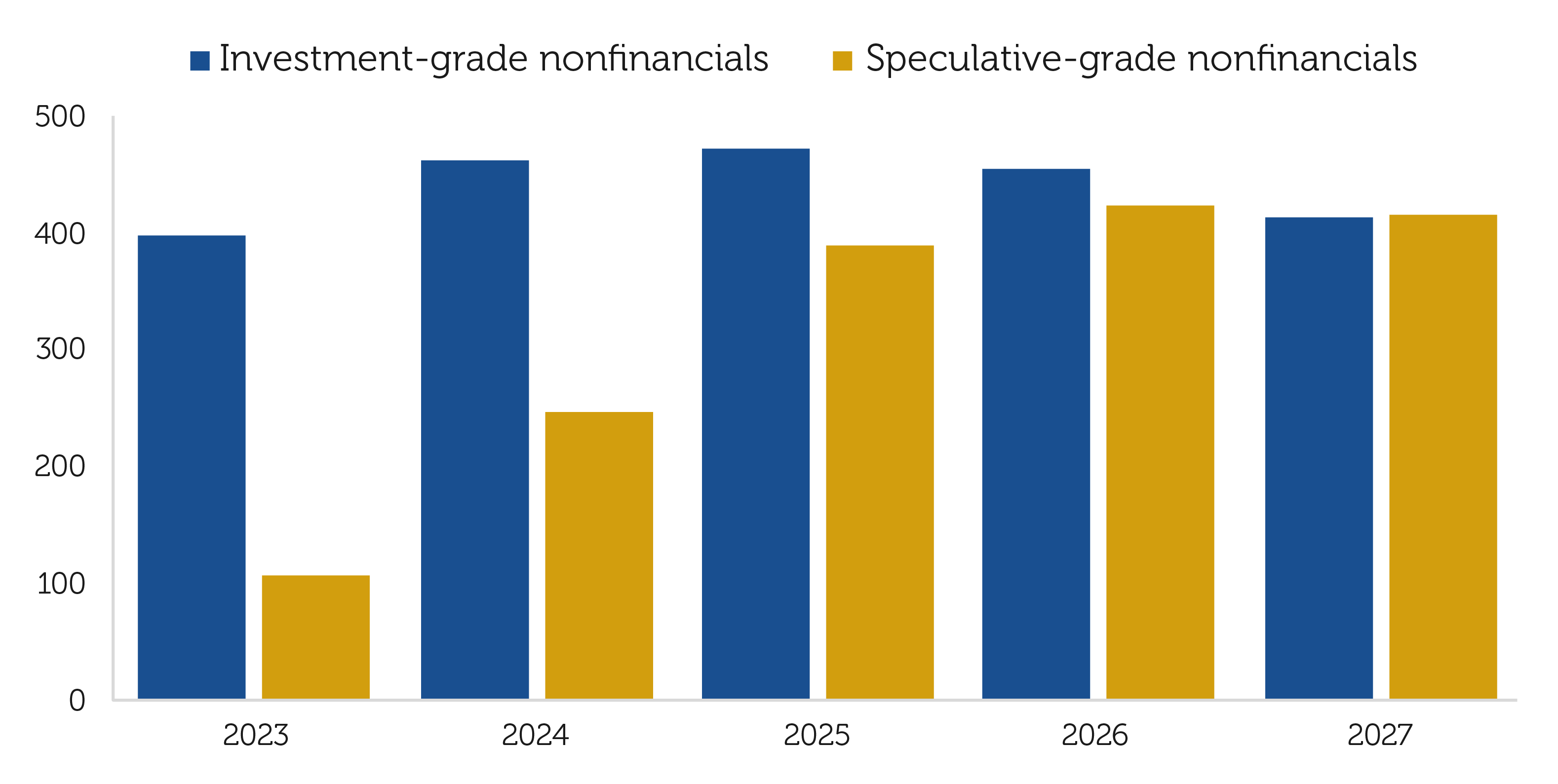

Maturity schedule for U.S. non-financial corporations ($B)

- High-yield bond spreads, as measured by the the ICE BofA US High Yield OAS Index, have compressed nearly 200 basis points over the last twelve months. Currently at ~4%, roughly in line with historical norms, spreads seem to be suggesting a soft economic landing is on the horizon.

- Markets may not be adequately pricing in a new normal of higher rates. Companies will struggle to refinance debts as cheaply as they could in the prior decade of ultra-low interest rates. This could have a significant impact on lower-quality issuers, who are confronting a surge in maturities over the next few years.

- We question whether stock and bond markets are discounting the lag effects of monetary tightening, which may have further to go. In our credit-driven economy, wider cracks would seemingly form the higher rates go and the longer they remain elevated.

Data as of Jan. 1, 2023.

Includes bonds, loans and revolving credit facilities that are rated by S&P Global Ratings. Excludes debt instruments that do not have a global scale rating.

Source: S&P Global Ratings Credit Research & Insights

© 2023 S&P Global.